2026 Software Playbook

Issue #91, Volume #3

SaaS’s Big Crash Is Setting Up A Massive Second Act

Inside today’s Daily Journal…

Essay: 2026 Software Playbook

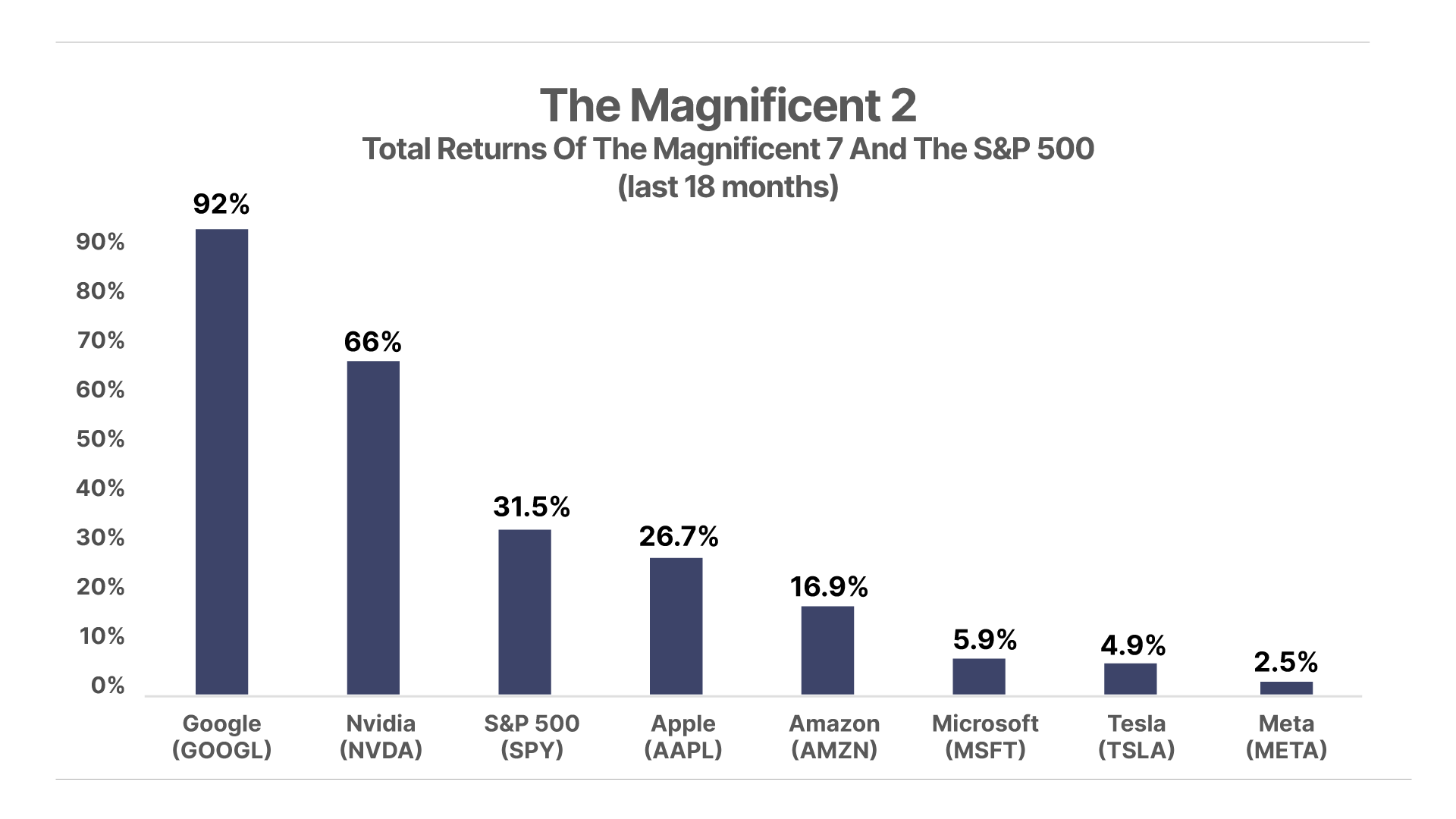

The Magnificent 2

Google partners with IBM and Palantir

Truckin’ just got more expensive

Chart Of The Day… Broadcom (AVGO)

Today’s Mailbag

Editor’s note: Porter has turned the Journal over to Porter & Co. analyst Jared Simons. Jared is part of the Complete Investor team as well as the architect of the weekly Sunday Stock Screen features. Today, he provides insights into the debate about whether artificial intelligence is killing the software industry.

Here’s Jared…

On February 3, the software sector experienced what traders at global investment bank Jefferies christened the “SaaSpocalypse” – an industry-crushing day for software-as-a-service (“SaaS”) stocks.

In a single trading session, $285 billion in market cap evaporated from enterprise software stocks. Within 30 days, the carnage widened to $2 trillion. At its April 10 trough, the iShares Expanded Tech-Software ETF (IGV) had fallen 35% from its 2025 high. On the individual company level, shares of ServiceNow (NOW) fell 65%, Adobe (ADBE) 51%, Salesforce (CRM) 54%, and Microsoft (MSFT) slid 34%.

The catalyst was specific – Anthropic’s Claude Cowork launch and a string of disappointing earnings – but the underlying repricing had been building for more than three years. Public SaaS growth rates had declined every single quarter since 2021. Artificial intelligence (“AI”) simply gave the market permission to mark down what fundamentals had been signaling all along.

The consensus narrative – “AI kills SaaS” – was expected. What’s actually happening is more nuanced and, for the right companies, far more bullish. You see, SaaS isn’t dying. It’s undergoing a forced metamorphosis from passive infrastructure into active intelligence. The companies that survive this paradigm shift will be more valuable than the old SaaS ever was.

This is the playbook for understanding who wins, who dies, and where the asymmetric opportunity lies.

1. The Bloomberg Paradox: Growing Value To Legacy

The Bear Case: Startups will use AI to build cheaper versions of Salesforce, the leading customer relationship management platform

The Reality: People love to call Salesforce a “legacy dinosaur,” but those people are missing the Bloomberg Effect. At Porter & Co., we don’t pay for the big-ticket Bloomberg terminal because we like the 1990s user interface. We pay because we’re held hostage. Our analysts have built so much proprietary logic and custom data-tracking into the terminal that ripping it out would kill our workflow.

Incumbents like Salesforce and ServiceNow own the “enterprise memory” – years of your company’s specific rules, data graphs, and institutional knowledge baked in. If you own the data and the habit, you are better positioned to deploy AI than any upstart fighting for access and distribution.

The early evidence – and the most recent quarter – validates this thesis. Salesforce closed fiscal 2026 with $41.5 billion in revenue, up 10% year-over-year, and its AI-driven Agentforce platform hit $800 million in annual recurring revenue (“ARR”), growing 169% with over 60% of Agentforce bookings coming from existing customer expansion. As of Q1 fiscal 2027 (reported May 27, 2026), Agentforce has crossed $1 billion in ARR. Quarterly revenue rose 13% to $11.13 billion, and management raised full-year FY27 guidance to $46 billion.

The installed base isn’t fleeing, rather it’s doubling down. Add the more than 28.6 trillion tokens processed to date (up 152% for the quarter) and 3.8 billion Agentic Work Units (“AWU”) delivered across Agentforce and Slack – AI executing real work inside the customer’s own data context – and that’s what’s keeping the newcomers away.

2. Expanding The Pie: The $13 Trillion Prize

The Bear Case: SaaS is a saturated market with no room for growth

The Reality: The market is fundamentally mispricing the opportunity. Global SaaS is a $400 billion sandbox. The U.S. labor market is a $13 trillion opportunity.

Traditional software was just a “filing cabinet” – a passive place where you recorded what humans did. The winners of this cycle are changing – they aren’t just storing data. They are the “brain” that receives a messy inbox of tasks and delivers that information to the critical stakeholders to more efficiently perform their job. When software stops being a tool and starts being the worker, it stops competing for the software budget and starts eating the $13 trillion labor budget.

The shift from Software-as-a-Service to Service-as-Software is the new thesis. Tax and business advisory firm Deloitte predicts that up to half of organizations will put more than 50% of their digital transformation budgets toward AI automation in 2026, with agentic AI investment reaching 75% of companies. Tech research firm Gartner projects that by 2030, 40% of enterprise SaaS spend will shift toward usage-, agent-, or outcome-based pricing. The addressable market isn’t shrinking. It’s exploding beyond what traditional SaaS ever captured.

3. The Margin Utopia Versus Compute Costs

The Bear Case: AI is too expensive to run – gross margins will collapse

The Reality: Token costs are falling 10x a year while the value of the outcome stays high. If a company can charge $20,000 for a legal task that used to cost $200,000 in human salary, and the computing cost is only $500, margins aren’t shrinking – they’re entering a Golden Age. This is why more companies are moving from “selling the infrastructure” to “monetizing the intelligence.”

4. The Seat-Based Extinction

The Bear Case: If AI replaces people, software companies lose their “per-user” revenue

The Reality: This is the biggest risk for laggards, but the biggest win for visionaries. The seat-based model is dead. The February selloff was a market-wide awakening to this structural flaw: when AI agents can do the work of 100 sales reps, you don’t need 100 Salesforce seats.

Salesforce rolled out AWUs as a new operational metric alongside ARR, signaling the industry’s shift from counting users to counting completed work – which is what AWUs measure. The transition is messy – even Salesforce CEO Marc Benioff acknowledged that customers pushed back on pure per-conversation pricing and want more flexibility – but the direction is clear. Companies that land this pricing pivot will be rewarded for the volume of work finished per employee rather than capped by headcount. That’s a larger addressable market, not a smaller one.

5. Own The Data And The Action

The Bear Case: Incumbents will bundle everything and crush startups

The Reality: Startups are winning at formation. New companies being born today aren’t even looking at the old guard. They’re starting with AI-native set-ups that manipulate data from day zero. While incumbents own the “hostages” – the Fortune 500 companies tethered to their products – startups are seeding the next generation of giants. On the surface, it looks like a two-sided race: incumbent innovation speed versus startup distribution speed.

But there’s a third front that neither side fully controls: the AI middleware layer. Renowned venture-capital firm Andreessen Horowitz (“a16z”) is actively funding startups that treat Salesforce and ServiceNow not as competitors to be replaced but as backend data layers to be wrapped with an AI-native interface.

a16z calls this the “system of action” – a governed AI layer that sits on top of the system of record, handling workflows, cross-system orchestration, and user-facing automation while the legacy platform underneath persists as a dumb-but-critical database. The risk for incumbents isn’t replacement. It’s disintermediation. If the user relationship migrates to that middleware, the incumbent keeps the recurring subscription revenue but loses the agentic pricing upside – the outcome- and credit-based models described above. If a company owns only the record layer, it becomes a toll road: valuable, but with stunted growth. The key to winning: Own both the record layer and the action layer.

The decisive question for the next several quarters is whether incumbents can open their action layer fast enough – and meter it well enough – to make the middleware a feature of their platform rather than what disintermediates them.

The 2026 Verdict: Intelligence Over Infrastructure

SaaS is not facing an existential death – rather, it is undergoing an evolution into an agentic paradigm. For incumbents, the future is a high-stakes race against distribution decay – they must prove they can leverage their proprietary data before their seat-based revenue models collapse. For startups, the mission is to create their own hostages, who have long protected the old guard.

For a decade, SaaS was a “magical” growth story of predictable, seat-driven ARR. Today, the market is aggressively de-rating those same companies from 35x cash flow down to 15x. The premium collapsed because the old valuation logic was broken by agentic AI.

The February crash wasn’t a knockout punch. It was a forced transition from passive systems of record to active systems of work. The companies that can make the change will capture a far larger addressable market than the old SaaS model ever imagined.

The few incumbents that own both the data layer and the action layer are converting a $400 billion software market into a claim on the $13 trillion labor market.

Tell us what you think of today’s Journal: porterstansberrydirect@gmail.com

Good investing,

Jared Simons

Miami, Florida

Presented By: Golden Portfolio

3 Things To Know Before We Go…

1. The Magnificent 7 is just OK. Since the start of 2025, five of the seven top tech companies have underperformed the S&P 500 – a sharp break from the all-for-one leadership of previous years. Only Complete Investor recommendations Nvidia (NVDA) – up 38.9% in 2025 – and Alphabet (GOOG) – up 65.4% – beat the index’s 16.4% return. For seven businesses that still drive a third of market cap, that concentration cuts both ways: a stumble in one or two leaders now moves the whole tape.

2. Google partners with IBM and Palantir to expand AI market share. Alphabet (GOOG) and IBM (IBM) have launched a dedicated Google Cloud Practice to deploy AI agents optimized for Google’s Gemini Enterprise AI platform. Simultaneously, Google has deeply integrated Gemini and BigQuery with Palantir Technologies’ (PLTR) AIP and Foundry platforms on the Google Cloud Marketplace, creating a powerful tool that allows corporations to send complex data directly into AI-driven workflows. Together, these complementary deals leverage IBM’s consulting and deployment expertise with Palantir’s robust data infrastructure, positioning Google’s Gemini as the foundational ecosystem for next-generation operational AI.

3. Trucking rates hit an all-time high – faster than ever. The National Truckload Index (“NTI”) registered a shipping cost of $3.71 per mile – recording a 29-week, $1.38 surge that took 43 weeks in 2020–21. Yet freight volumes have shrunk for 14 straight quarters, as the Trump administration’s new crackdown on commercial licenses is pulling immigrants off the road. This shortage pushes inflation higher – the kind that gets baked into the price of everything on the shelf.

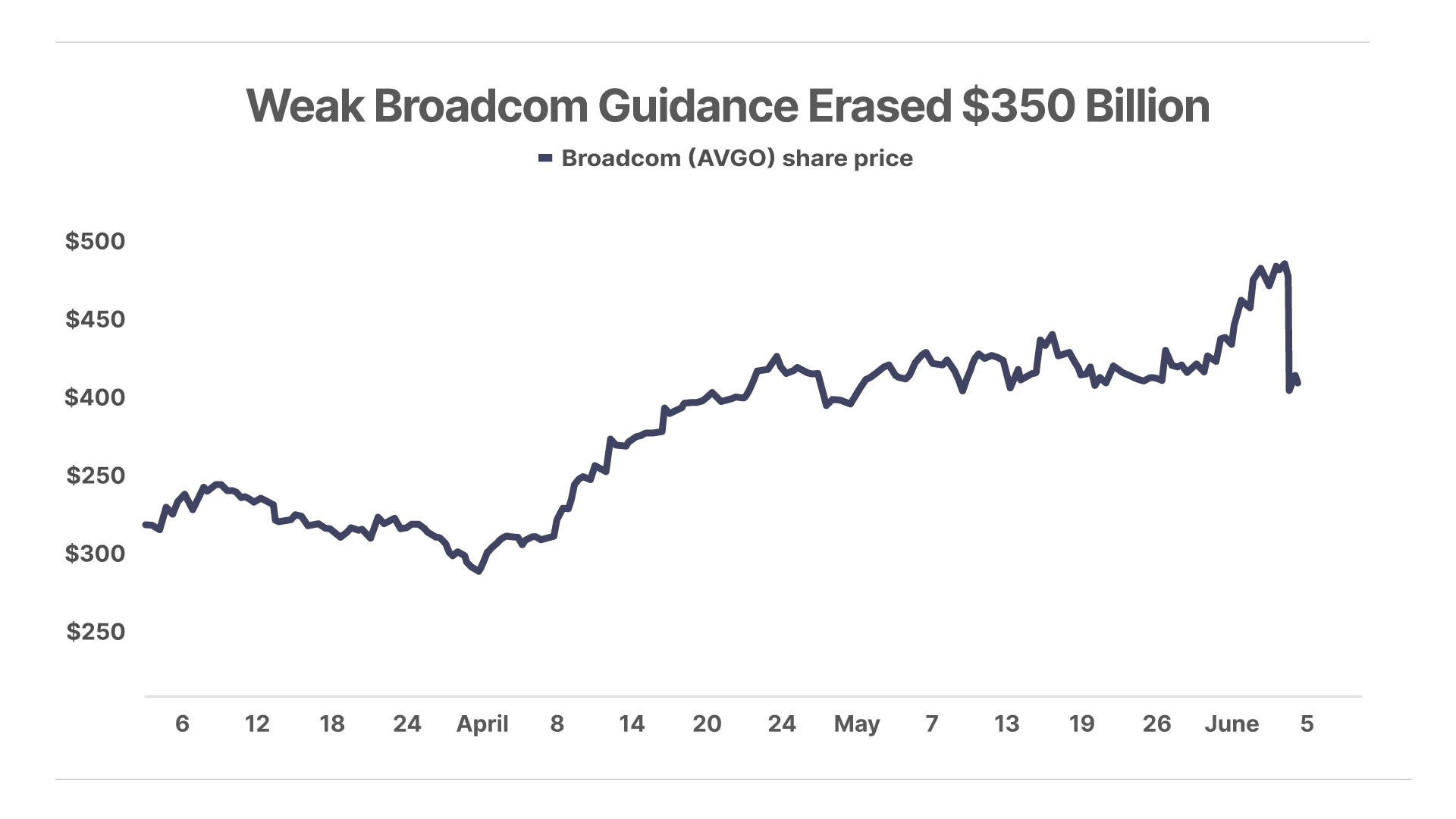

Chart Of The Day… Broadcom (AVGO)

Shares of AI chip designer Broadcom (AVGO) plunged 15% today despite blow-out Q2 earnings, after the company forecast weaker-than-expected Q3 revenue. With expectations running so high for AI-related companies, any hiccup can cause shares to tumble.

Mailbag

“2029: The End Of America”

Allan S. writes:

Hi Porter – I have just read your new book 2029: The End Of America on Kindle and found it both instructive and thought provoking – particularly with the historical perspective. I do not read it as an American but as a Brit, seeing in my own country many of the social trends you describe and I am very aware of more local economic and political developments that perhaps may lead us toward a precipice a little earlier than the one you describe. My portfolio is far more globally diversified than the ones you describe but in this very closely linked investment world in which an event in Japan can impact the S&P 500 within hours, I think the structures you propose can be as relevant to me as any American investor. Thank you for your insight and guidance.

“The Honeycomb Portfolio”

Wayne S. writes:

I agree with your Honeycomb portfolio thesis that incorporates a diversified portfolio divided among differing investment assets. I suggest one alternative investment to replace bonds as a safe long-term investment: dry grain farm land. The land investment should have a long, consecutive-year profit crop history. In a good location, the land will hold its value and grow over time, driven by food-cost inflation and spin-off a modest annual income into perpetuity.

“The Move Into Crypto”

John E. writes:

Hi Justin,

Interesting to hear Porter & Co is moving into the crypto space following the utter carnage of the last few years. Hopefully you get to learn from the mistakes made by those who tried and failed before.

If earlier (including those still around) crypto newsletters failed, it was not properly getting their heads around the Value Proposition for each crypto token. Too often they would analyze the potential of a given project, without paying enough attention to exactly how the token will generate value from that project if it proved successful.

We all understand the value proposition for an equity: standardized rules that grant the holder of the equity with part-ownership of the company’s cashflows and net assets. No such thing exists in crypto. I’m hearing too often these days: “I don’t understand how such and such token generates value from the underlying project.” I believe the market has largely woken up to this problem, and this partially explains why altcoins have been such a disaster.

Wishing you the very best.